Going Into the Field First

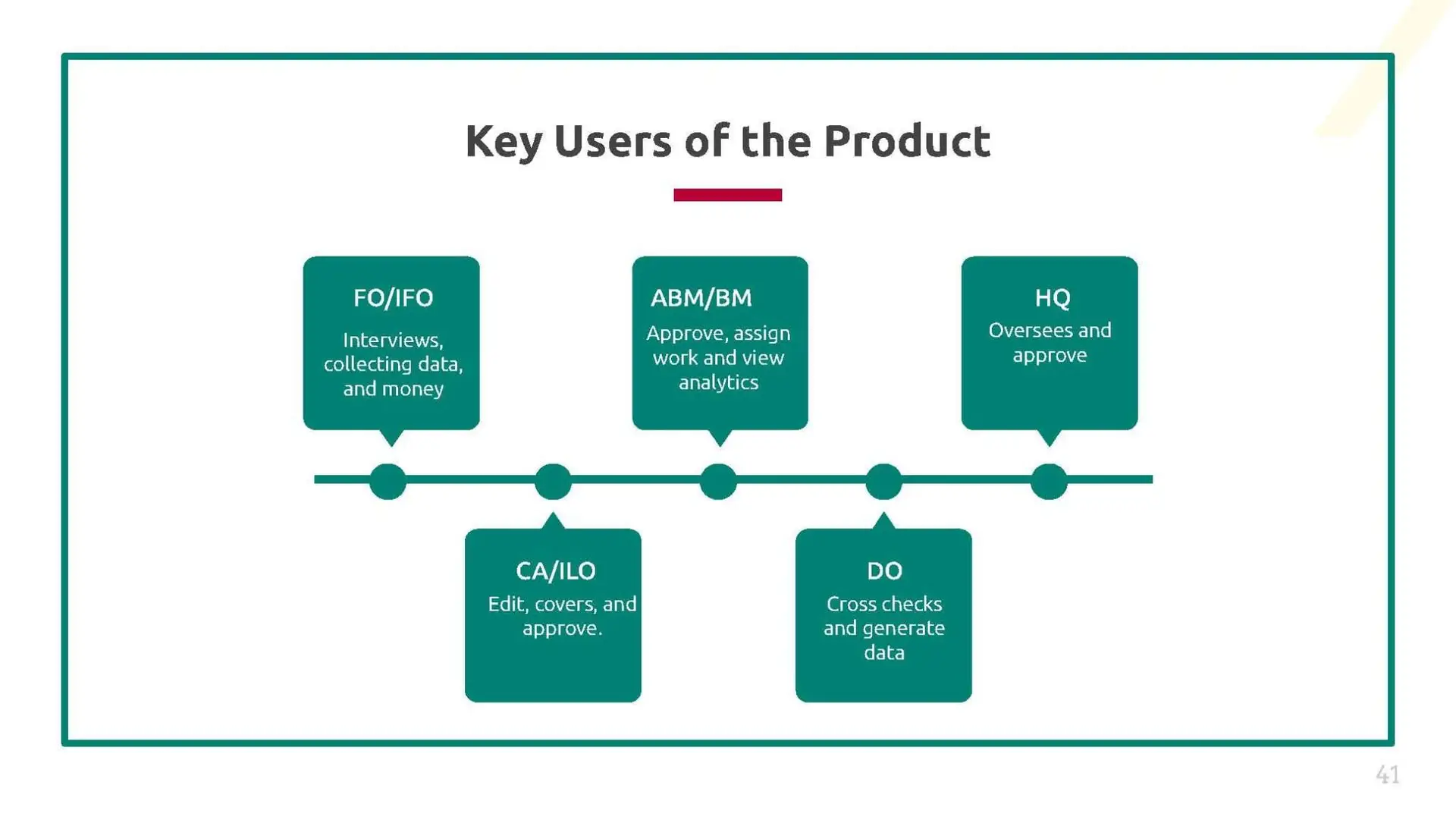

I led research using ethnographic methods — one-on-one interviews and contextual inquiry with the people living inside these broken workflows every day. Six distinct roles across the organization: regional managers, branch managers, credit advisors, data operators, and both individual and group loan field officers.

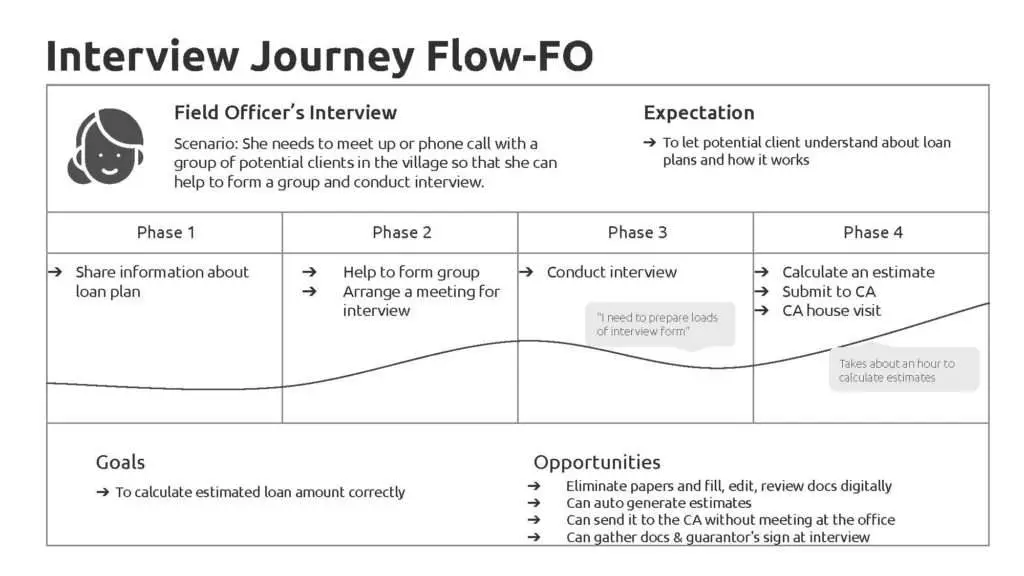

Each role had a different relationship with the paper problem. Officers felt it in their legs — multiple home visits per applicant just to gather and verify information. Managers felt it in their visibility — no real-time view of where applications stood in the pipeline. Data operators felt it in their hands — re-keying handwritten forms into systems, catching errors that never should have existed.

The deeper issue wasn’t paper. It was that the entire loan pipeline had been built around the assumption that humans would manually bridge every gap.

100% digital in their business operations, and to go paperless and to reduce human errors.

Aim

To drive a sustainable and scalable MFI by helping Myanmar people grow their own businesses.

Product Goal